Value

Track your spending, optimize your budget and improve savings to reach those goals that truly matter to you

01

Context

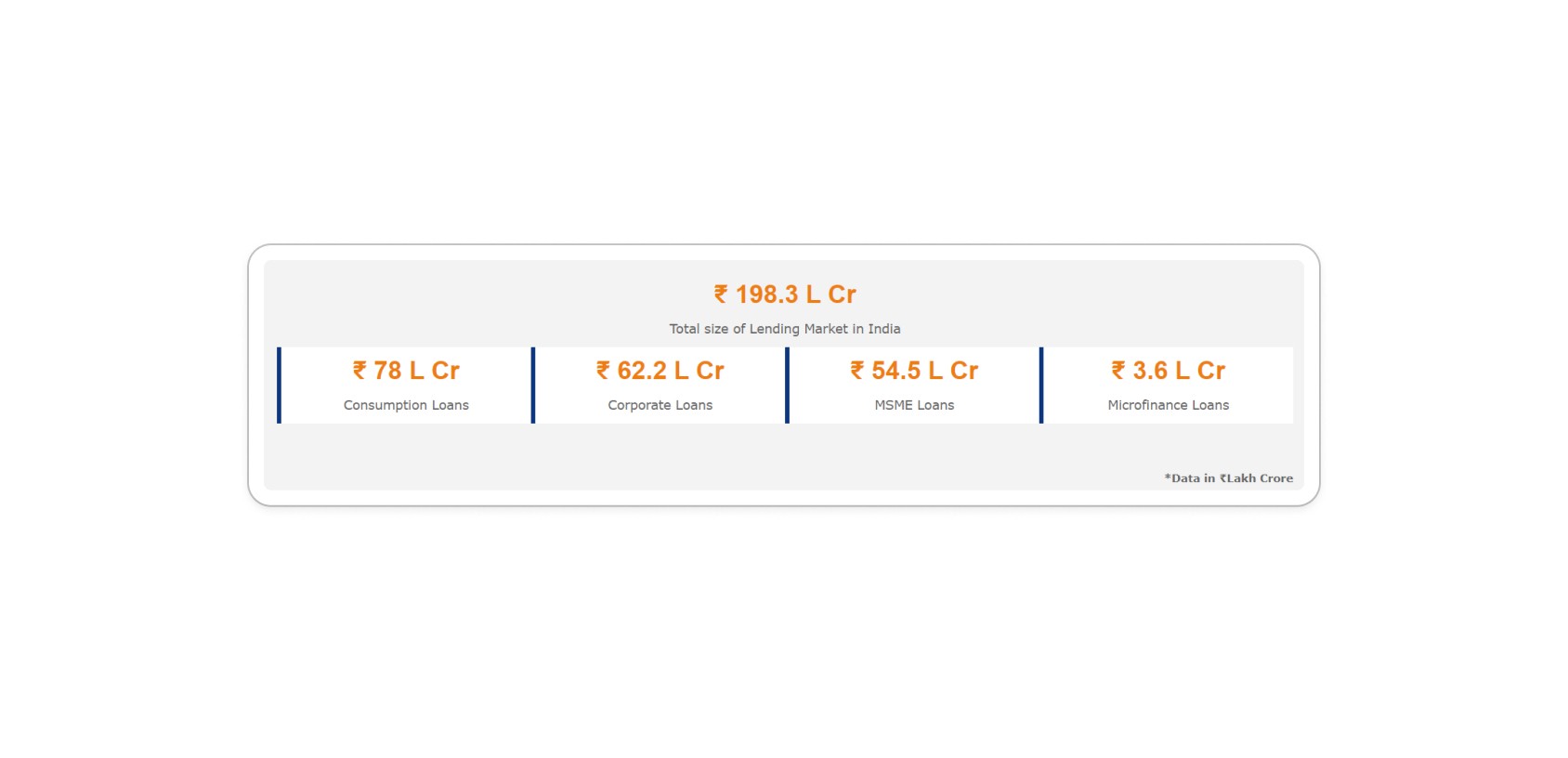

In today’s connected, consumerist lifestyle, one can easily be overwhelmed by the complexity and time burden of managing personal finances.

We have various services and infrastructures maintaining fragments of our financial footprint – banks, UPI apps, all the various wallets, investment portfolios, and so many more micro-services.

Usually, the financial-unsavvy person would get overloaded by this information and tend to ignore it altogether.

Early Assumptions

I started my research by writing down some basic assumptions I have on the target demographic and the problems they might be facing

02

Secondary Research

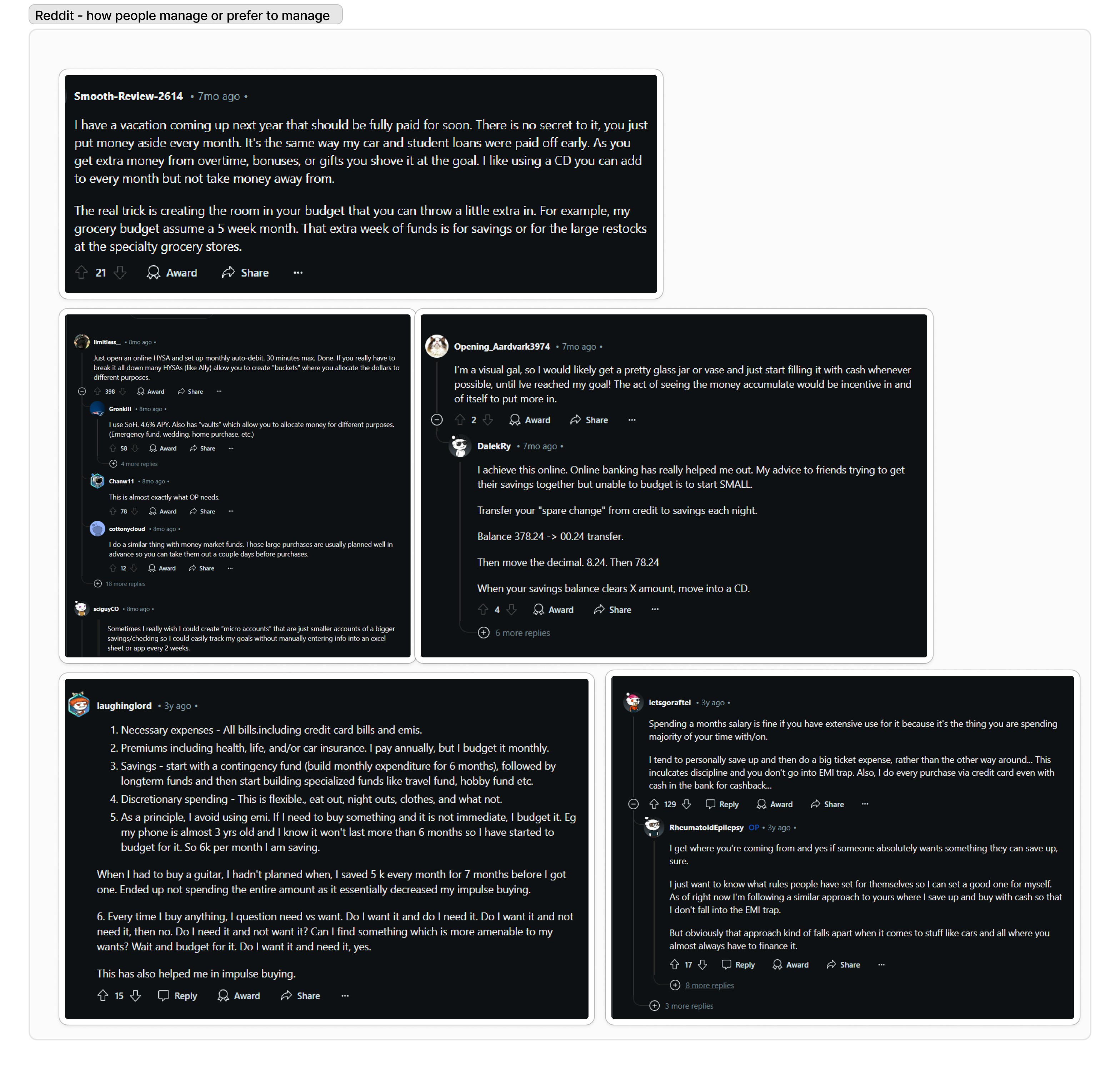

I searched for articles and studies related to how people manage their money to figure out common user behaviors and also examined conversations happening in spaces like Reddit to know the best practices they recommend or adopt. Following are the insights

Users shift money to other accounts meant for savings and goals

use of a vault-like feature - allocating money for different purposes

Wait, budget, and save - common advice for buying large purchases

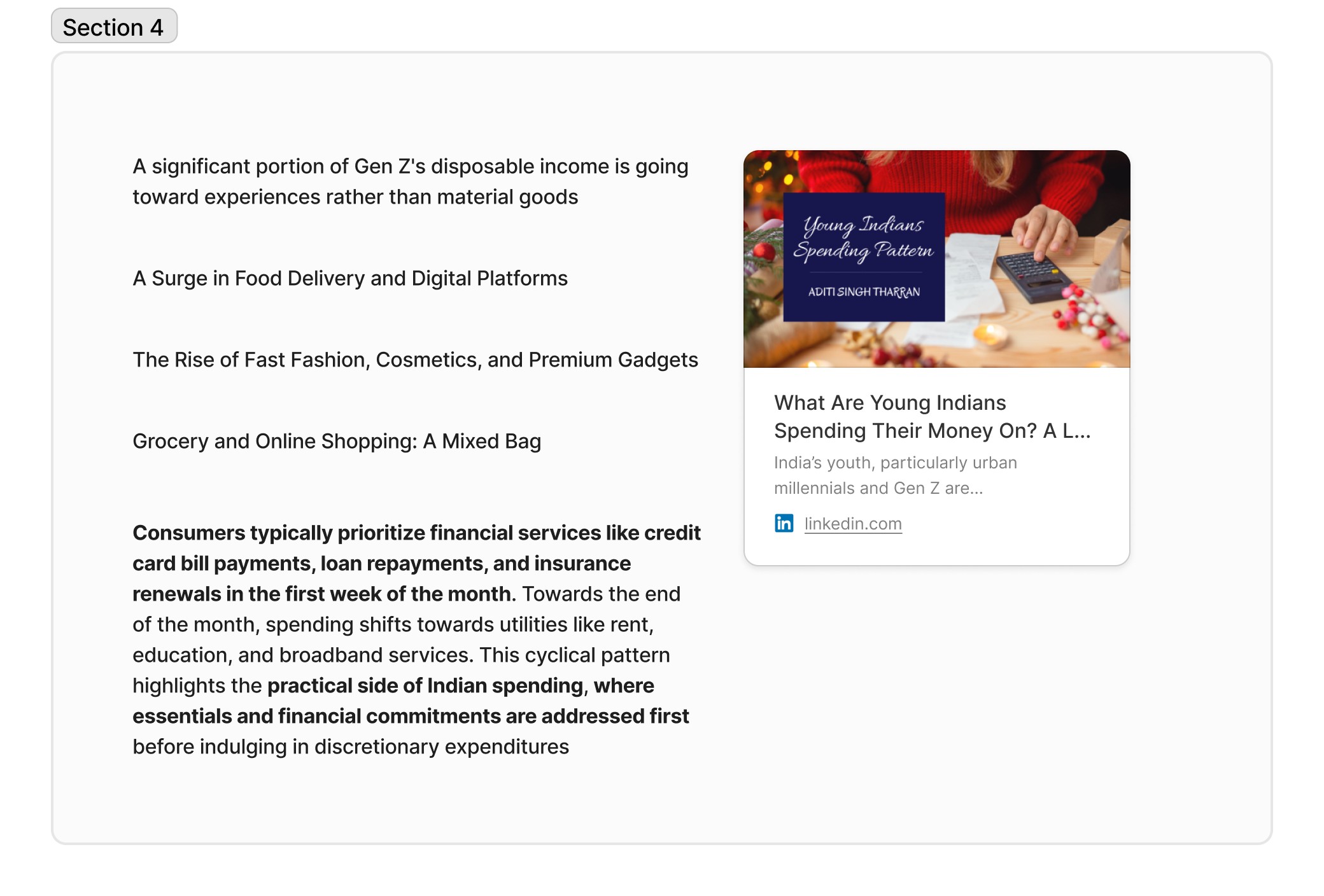

Rising expenditure in households

Essentials and financial commitments are addressed first before discretionary expenditures

03

Competitive Analysis

What I found out was many a product had too many functionalities. They lacked a singular focus on helping users manage their money better. Mostly, everything is oriented toward spending. The UPI apps we use, fintech products like Cred, Slice, Phonepe, and Google pay - all want us to spend money through their platform. They made it sophisticatedly easy to do so.

But in those lines of one tap payment - from online shopping to Kirana stores, somewhere we forgot to keep track, keep a log on that one crucial thing -- do our expenditures match with what we truly value?

04

Primary Research

Except for Fold money, all else focuses on making the user spend through their app.

Now with rising expenditures shouldn’t budgeting features be a norm?

How do users budget these days? Or do they even now? This brings us to our primary research.

User Survey responses ( Pain points )

Lack of a clear budget: Almost half of the respondents mentioned lack of a clear budget as a hindrance to saving and investing

Lack of financial knowledge

Difficulty tracking expenses

All have issues with prioritizing savings and investing

SIP, Mutual Funds, and Stocks are favorite investing options among youngsters

User Interviews

I interviewed 4 people and the following were the insights

Balancing financial vs personal goals: 4 out of 4 participants mentioned difficulty balancing financial goals with personal or social experiences.

Feel confident: 3 out of 4 participants said they want to feel confident about managing finances and make rational spending decisions to pursue personal interests.

Tracking and Budgeting: 2 out of 4 participants said they struggle with allocating budgets and tracking spending without feeling overwhelmed or anxious.

Expense tagging and categorization: 2 out of 4 participants said they forgot to tag expenses or categorize them properly, leading to confusion at the end of the month.

05

User Persona

Collecting all our insights from user research, I crafted a coherent user persona and charted a user journey map for the same

06

Breaking down the problem

I broke down the problems into high-level goal and the why behind it

Redefined Problem Statement

How might we help users establish clear and personalized budgets that provide visibility and control over their spending—so they can manage their finances confidently while still enjoying the things that matter most?

07

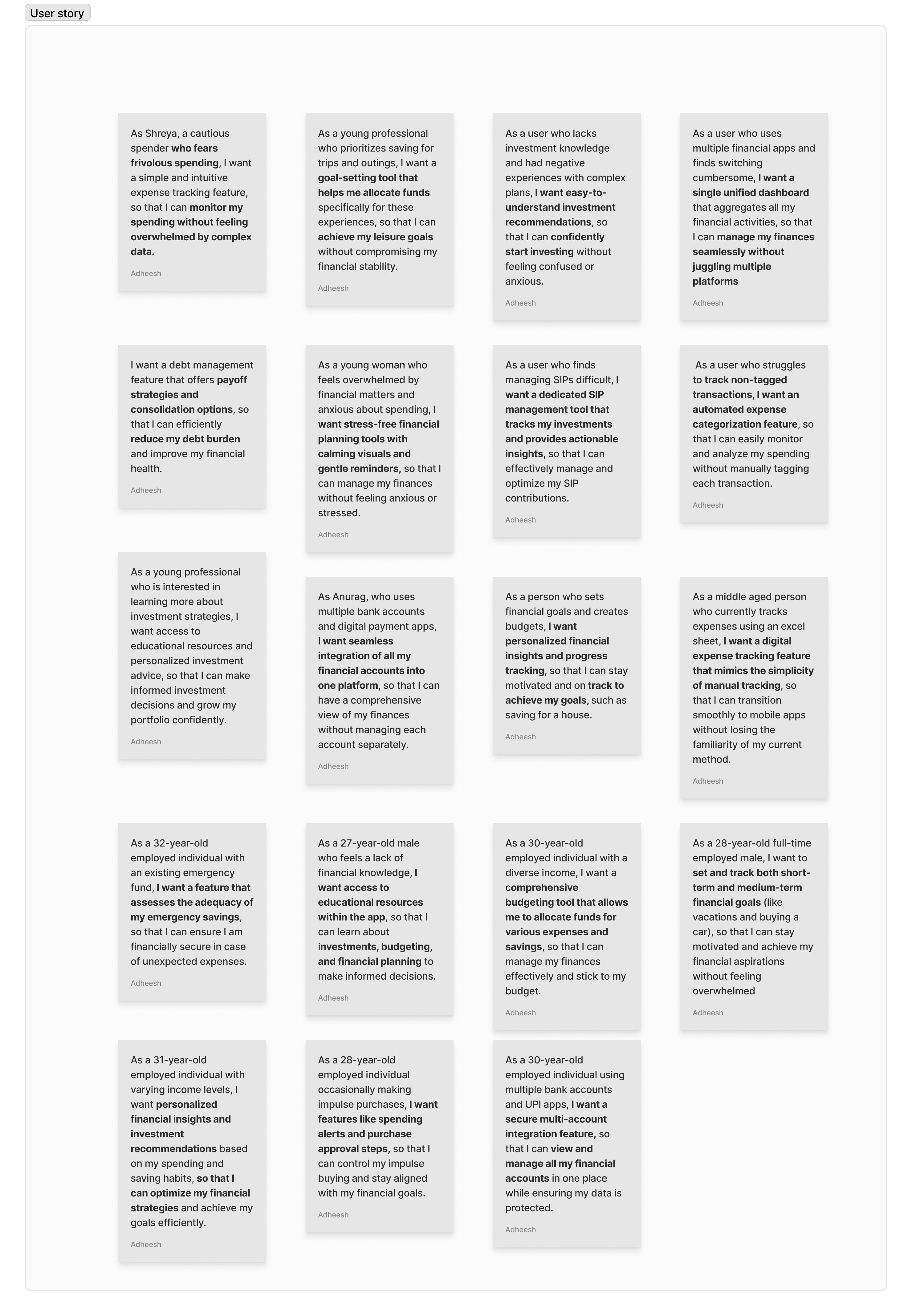

Curating user stories

Curated user stories w.r.t the persona and data gathered from research

08

Prioritizing user stories

I took the curated user stories which were arrived at by analyzing research data, and put them across an impact effort matrix

Chosen user stories to pursue :

"As a cautious spender who fears frivolous spending, I want a simple and intuitive expense tracking feature, so that I can monitor my spending without feeling overwhelmed by complex data."

I want stress-free financial planning tools with calming visuals and gentle reminders so that I can manage my finances without feeling anxious or stressed.

09

Ideation via Information Architecture

From the effort impact matrix, I've finalized the user story for the cautious spender and derived an information architecture that suits the flow for a budgeting app

10

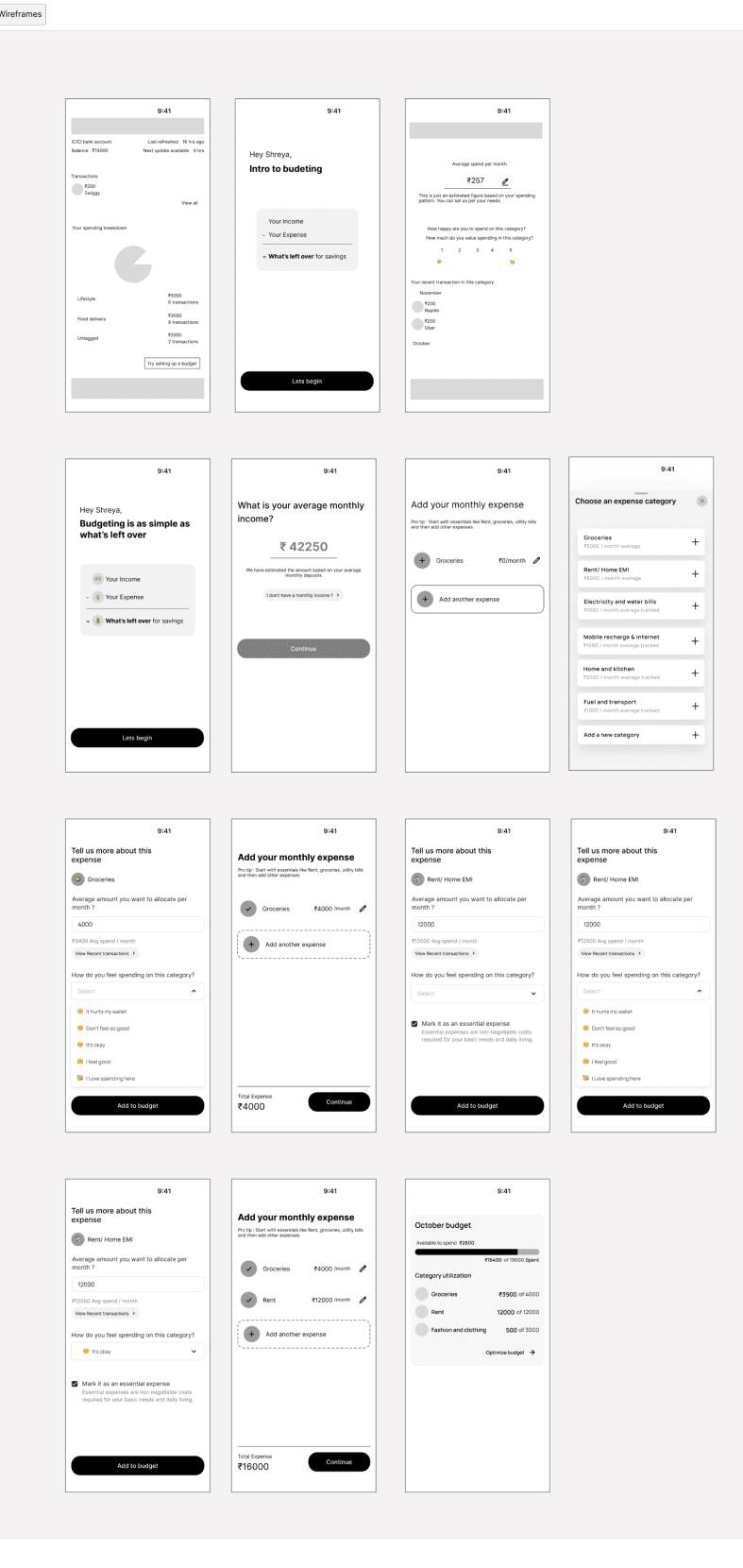

Early Wireframes and low fid prototyping

Following the above information architecture and some reference from budgeting apps I've created some wireframes and prototyping

11

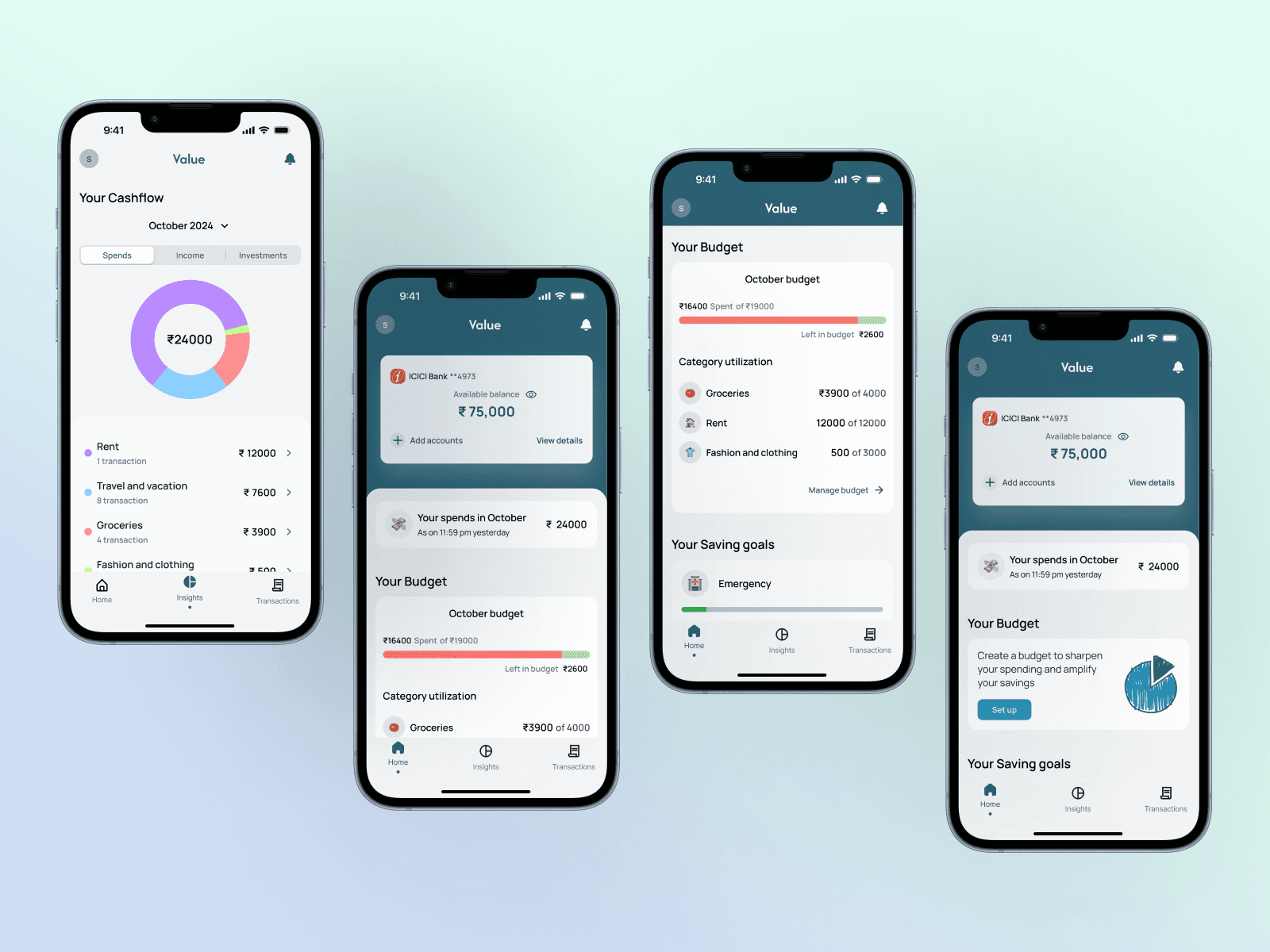

Visual Design and High Fidelity

My initial high fidelity wasn't following current UI standards; therefore, after many design iterations, I came up with the following screens

12

Next Iteration Considerations

Incorporate Personalized Insights

Add spending trends and suggestions based on past months' data to help users optimize future budgets.Goal-to-Budget Integration

Develop dynamic links between goals and budgets, suggesting automatic reallocation when a user reaches certain milestones (e.g., reducing dining expenses to boost savings)Weekly Budget Check-ins

Offer bite-sized check-ins that suggest adjustments or give a progress summary to keep users engaged without overwhelming them.:

13

Potential Pitfalls

Zero Based budgeting not introduced

Users will still feel confused about the possibility of spending from bank savings and still not affecting the budget.

Emotional Spending Not Fully Addressed:

Users might still prioritize social or impulsive spending, leading to budget deviations.

Final thoughts and summary

As far as simplifying personal finance is considered it’s as follows

Know what your goals are

Keep track of your spending

Optimize your budget

Improve savings and achieve goals faster